China Decoded: Inside the “Six-Network” Mega-Project

The Big Picture: China’s $1 Trillion Infrastructure Pivot

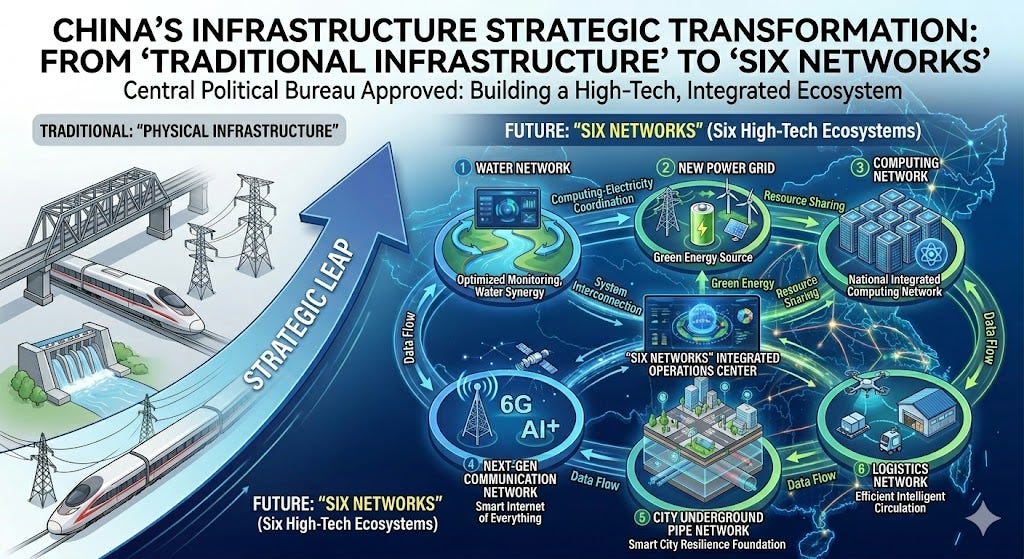

The CPC’s Central Political Bureau has greenlit a strategic overhaul of China’s backbone, transitioning from traditional “bricks and mortar” to a high-tech, integrated ecosystem known as the “Six Networks” (六张网). “加强水网、新型电网、算力网、新一代通信网、城市地下管网、物流网等规划建设。推动条件成熟的重大工程项目开工。”

According to China’s state media, Economic Daily (经济日报), with an estimated 7 trillion y…