Tax Bills, the Tomato Crisis, and Lost Love—A Micro-Level Revelation of the UK's Decade of Brexit

In September 2025, as I boarded my flight to Beijing at London Heathrow Airport, I looked back on my more than six years as a foreign correspondent in the UK, from 2019 to 2025. In that time, the UK experienced four Prime Ministers, two monarchs, and one pandemic. Outside the black door of 10 Downing Street, Rishi Sunak resigned in the rain—a scene full of tragedy; at that very same door, successive Chancellors of the Exchequer held up their Red Boxes, smiling confidently at the cameras, full of high spirits; yet, no matter how the masters of Downing Street came and went, none stayed longer than a cat named Larry.

In the summer of 2026, the UK changed its Prime Minister once again. Keir Starmer stepped down in dismay, becoming the sixth Prime Minister to fall in the ten years since the Brexit referendum. At this very moment, the highly popular “King of the North,” former Mayor of Manchester Andy Burnham, is confidently eyeing the Prime Minister’s seat.

In Westminster, politicians and political commentators are accustomed to blaming the frequent turnover of Prime Ministers on PR disasters, party infighting, or terrible election strategies. I witnessed, experienced, and reported on what happened in this country for most of the decade following Brexit. As a foreigner who once lived in London, when I tried to understand why this country, once renowned for its political stability, had become seemingly “ungovernable,” I found the answers not in parliamentary debates, but in a few everyday trivialities I personally experienced. Behind the endlessly spinning “revolving door” of 10 Downing Street, the structural decline of the macroeconomy and the throes of geopolitics have quietly rewritten the fates of ordinary people.

The Glaring Numbers on the HMRC Tax Bill: Downing Street Locked by the Bond Market

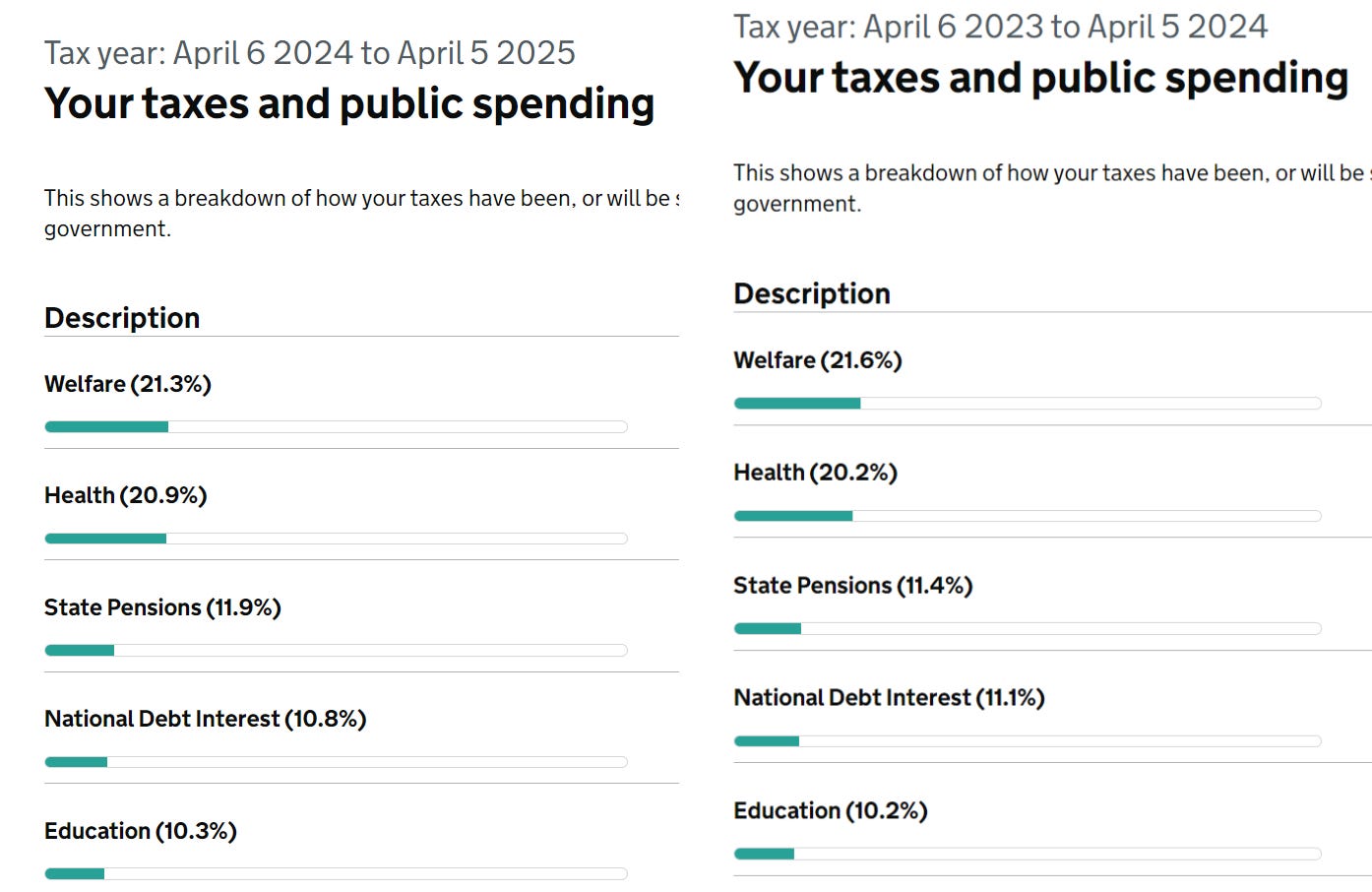

When I finished my term and was preparing to leave the UK, I logged onto the HM Revenue and Customs (HMRC) website to see exactly where the taxes I had paid over the years had gone. In the system-generated bar chart showing the allocation of my personal tax contributions, the fourth largest government expense—ranking right after welfare, healthcare, and pensions—was shockingly “National Debt Interest.”

I always knew that the most important indicator of a nation’s rise and fall is “money,” but I never expected to touch the economic pulse of this country in such a manner.

When the interest a country has to pay annually on its national debt approaches the total amount spent on nationwide pensions, it inevitably surprises those of us from a culture that “loves saving and hates owing.” That glaring number instantly made me realize the greatest illusion in British politics in recent years: whether it was Liz Truss’s disastrous “mini-budget” or Keir Starmer’s attempt to plug the fiscal black hole with tax hikes, every new government was merely dancing in heavy shackles. When massive portions of the budget are forced into paying debt interest, the funds available for the government to invest, stimulate growth, or repair public services are severely squeezed. Brexit itself has imposed a heavy structural headwind on this fragile economic foundation.

According to authoritative joint research conducted by the Stanford Institute for Economic Policy Research (SIEPR), the National Bureau of Economic Research (NBER), and the Bank of England, the Brexit process has caused a long-term shrinkage of the UK’s GDP by 6% to 8%. According to the latest figures from the Office for National Statistics, by May 2026, the UK’s public sector net debt had reached 95.10% of its Gross Domestic Product (GDP), requiring £111 billion in interest payments alone each year. In 2025, the yield on 30-year UK government bonds briefly hit 5.5%, marking a 25-year high.

The fiscal policies tucked inside the Chancellor’s Red Box must be meticulously calculated: how to bring in more money, how to achieve more while spending less, and how to borrow more money at lower interest rates. This explains why anyone—from Starmer to any future Prime Minister—cannot easily flex their muscles. The UK is no longer ruled solely by the House of Commons, but also by the cold, hard “bond market.” Any stimulus plan lacking financial backing will be met with ruthless market sell-offs. The national debt interest on that HMRC bill is the fiscal noose tightening around the neck of every British Prime Minister.

The “Tomato Crisis”: Trade Barriers Whitewashed by Lies